Currently, 300,000 elderly people in retirement live in poverty, which represents 17% of retirees. These individuals survive on less than 2,000 CHF per month.

Shocking, right? I understand, it struck me too.

In a country like Switzerland, one might think they are safe from any kind of financial hardship. Unfortunately, that’s not the case.

That’s why the actions you take now, after reading this article, can help you secure your retirement and may even allow you to take early retirement.

3-2-1, let’s go!

Let’s start with the basics

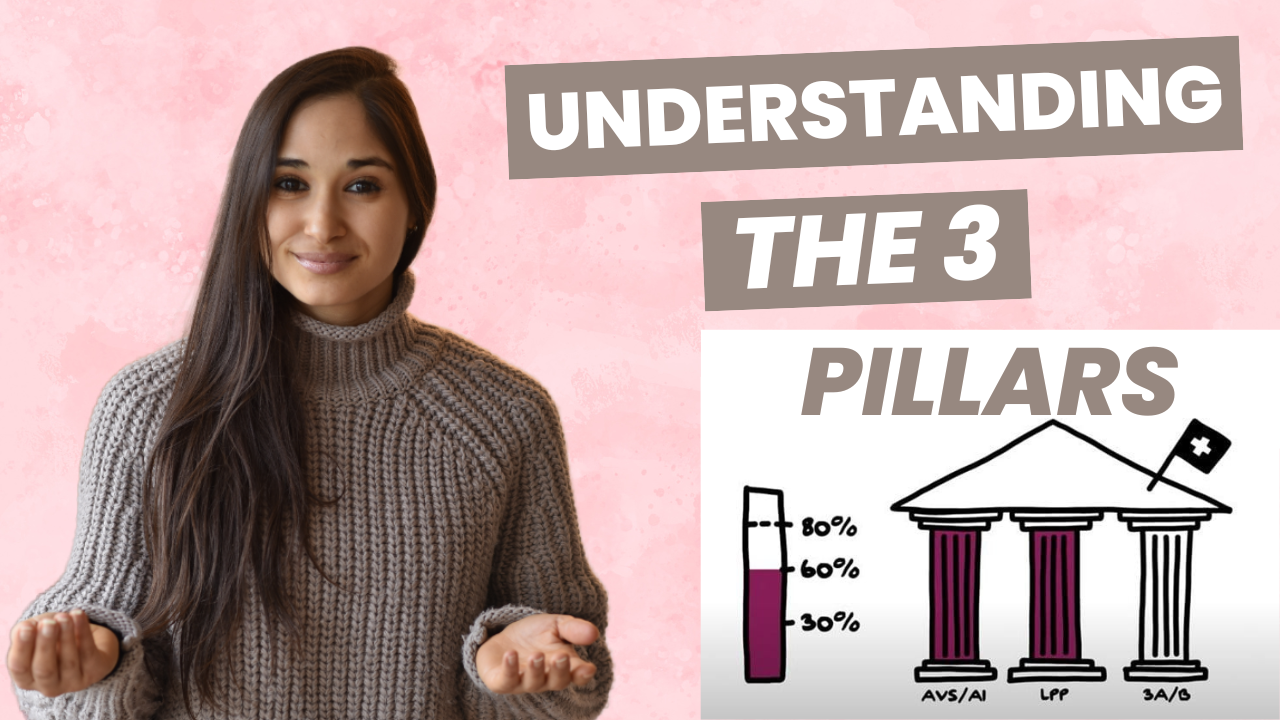

To understand why it’s important to invest for your retirement, we need to take a closer look at the Swiss pension system. This system is also known as the 3-pillar system. The first two pillars are mandatory, while the third is optional. However, the third pillar is very important, and you’ll soon understand why.

What is the 1st pillar?

The 1st pillar is simply the AVS (Old Age and Survivors Insurance), which is part of the monthly deductions from your gross income.

This is a social insurance that guarantees a minimum income to anyone who has worked and contributed in Switzerland. At retirement, you will receive a monthly pension, capped between a minimum and maximum amount. The amount of this pension mainly depends on the number of contribution years and the income on which contributions were made. The minimum pension for a single person currently amounts to 1,225 CHF per month, and the maximum pension is 2,450 CHF.

To receive the maximum pension, currently set at 2,450 CHF, you would need 44 years of contributions with an average annual income of 88,200 CHF.

The average salary is the sum of all the salaries you’ve earned, divided by the number of years you’ve worked. Once your average salary is determined, you can refer to a table called the “Scale 44” to find out your pension amount, which you can find here.

But beware: if you are married or in a registered partnership, your combined pension is limited to 150% of the individual maximum pension, which is 3,750 CHF for two people—admittedly not a lot.

Now let’s talk about contributions. As long as you’re employed, no problem! The issue arises when you are unemployed and over 21 years old. You will then need to contact the compensation office to avoid contribution gaps, which would reduce your pension by about 2.3% for each year without contributions. Note that you have 5 years to fill in each contribution gap, so be sure to regularly check your situation by requesting your individual account statement!

Now, let’s look at the 2nd pillar

Also known as the LPP (Occupational Pension Plan), its purpose is to help you maintain your current standard of living during retirement. By combining these first two pillars, it is estimated that you will reach 50% to 70% of your last salary.

To contribute to the LPP, you must earn more than 22,050 CHF per year and be at least 25 years old. Once these conditions are met, you and your employer will contribute a percentage of your income to your 2nd pillar account, and this percentage is determined solely by your age. These figures represent the legal minimum. If your employer is required to contribute at least as much as you do, some employers may offer better conditions, known as the supplemental portion.

Are the 1st and 2nd pillars really enough?

At this point, you might be thinking, “50% to 70% of my salary, that’s chill—it’s more than enough!” Well, NO!

One problem with the 2nd pillar is that you can withdraw it partially or fully for certain life events, such as buying a home, permanently leaving Switzerland, or starting your own business. And what you withdraw for these events is what you’ll have less of in retirement.

Also, keep in mind that these are minimum amounts, PROVIDED that you have worked 100% your entire life. But as more of us choose to work part-time, take 6 months to a year off to travel, or stop working for a period after childbirth, you see the problem. The risk of poverty is indeed higher among women. In 2024, women still make up the vast majority of part-time workers at 56%, compared to only 16% for men.

And then, retirement doesn’t mean no more taxes… All pensions received from the 1st and 2nd pillars are taxable as income. For example, if an average-income person in Switzerland retires at 65, they will receive an AVS pension of 25,000 CHF + a LPP pension of 25,000 CHF, resulting in a total income of 50,000 CHF per year. Of this 50,000 CHF, they will have to pay about 9,500 CHF in annual taxes if they choose to take the 2nd pillar in the form of a pension.

Of course, they could also choose to take their 2nd pillar as a lump sum payment and pay a one-time tax. If you opt for the lump sum withdrawal for the 2nd pillar, you will have to pay a one-time tax upon withdrawal, calculated based on your family situation and your municipality of residence. In the example above, upon retirement at age 65, this person could withdraw a capital of 425,000 CHF before taxes, which would turn into 370,000 CHF after taxes.

The third option is a mix of the first two: withdraw 50% as a pension and 50% as a lump sum. This option offers some security with the lifetime pension and a significant capital to fund your projects. As with the other options, a one-time tax will be payable upon withdrawal.

When it comes to the amounts received from the first two pillars, they are not enough to fully enjoy retirement. But there are several tips to rectify the situation 😉

Tips for a better retirement

First, you can request a free account statement from the cantonal AVS compensation office and calculate your future pension. If you find that you’re missing contribution years, it is possible to make retroactive payments for the missing years (up to 5 years), provided you were eligible for AVS coverage.

As for the 2nd pillar, the pension amount is listed on the certificate you receive annually. You will also find the amount available for purchasing additional contribution years in the 2nd pillar (which are deductible in your tax return!).

These purchases help to fill gaps caused by a career break or a reduction in work hours. It’s a solution that both reduces your pension shortfall and lowers your taxable income, as the purchases are tax-deductible from your taxable income. However, there’s a drawback in my view: the return is… about 2% annually… For this reason, I prefer to invest in the 3rd pillar.

The 3rd pillar to the rescue

The Swiss pension system includes a 3rd pillar, which is private and optional, designed to fill pension gaps. More specifically, there are two types of 3rd pillars.

First, the pillar 3a, also known as the tied 3rd pillar. It allows you to contribute up to 7,056 CHF per year if you’re employed, and up to 20% of your net income, with a maximum of 35,280 CHF, if you’re self-employed. The amazing thing is that these amounts are deductible from your taxable income, giving you significant tax savings in addition to improving your retirement benefits. For example, with an income of 80,000 CHF without the 3rd pillar, a person pays 10,600 CHF in taxes in the canton of Fribourg. By saving the maximum allowed of 7,056 CHF in a 3a account, their taxes would be about 8,800 CHF. This represents a tax saving of about 1,800 CHF per year.

This pillar is called “tied” because it can only be withdrawn under certain conditions. These conditions include retirement, purchasing a primary residence, a disability over ⅔, permanently leaving Switzerland, or starting your own business. Note that withdrawing from the 3rd pillar involves an exit tax, similar to the 2nd pillar.

The 3b pillar, on the other hand, is also called the free 3rd pillar. It offers more flexibility in contribution amounts and withdrawal terms, but it is only tax-deductible in certain cantons, namely Fribourg and Geneva.

Interested in opening a 3rd pillar? Know that there are now hundreds of service providers offering private pension products, both in banks and insurance companies. Each can have its advantages and disadvantages, such as guaranteed interest rates, flexibility in payments, or the option to invest the funds. To determine the best provider and product for you, it depends on your situation, needs, plans, etc.

My top 3rd pillar choices are those that allow me to invest my money in the stock market to benefit from compound interest. Depending on the financial institution where you have your 3a pillar, you can invest in pension funds, ETFs, index funds, stocks, bonds, and more recently, in cryptocurrencies.

It’s easy to conclude a private pension contract, but it’s harder to fully understand which products best suit us, especially in this ocean of possibilities. So let’s book a free 15-minutes call with me here, so that we can review your situation together and find the best option for you.

Have a great day and…

To your peaceful retirement!